Exclusive Military Benefits That Make Homeownership More Affordable

Military service members, veterans, and eligible surviving spouses face unique challenges when purchasing homes or refinancing existing mortgages. Frequent relocations, deployment schedules, and varied income structures complicate traditional financing approaches. VA loans provide a specialized solution—offering competitive financing structures with flexible initial investment options, enabling qualified military families to purchase homes, refinance existing mortgages, or access home equity with terms designed specifically for those who've served. This comprehensive guide reveals how eligible borrowers can leverage VA loan benefits, navigate the Certificate of Eligibility process, and maximize the advantages earned through military service.

Key details you'll discover:

- How VA loan guarantees work to eliminate the need for private mortgage insurance while protecting lenders against default losses (VA Home Loans Overview)

- Certificate of Eligibility requirements that qualify active duty service members, veterans, National Guard, Reservists, and certain surviving spouses (VA Eligibility Requirements)

- Funding fee structures that vary based on service type, loan purpose, and whether you're a first-time or subsequent VA loan user (VA Funding Fee Chart)

- Property condition standards that mandate move-in ready homes meeting minimum property requirements for safety and habitability (VA Minimum Property Requirements)

- Occupancy requirements mandating primary residence use within 60 days of closing with limited exceptions for military orders

- Entitlement restoration processes that allow veterans to reuse VA loan benefits after selling previous VA-financed properties

- Residual income calculations unique to VA loans that assess affordability based on family size and regional living costs

- Specialized refinance options including standard rate-and-term refinancing, cash-out refinancing, and the streamlined IRRRL program

Ready to explore your options? Schedule a call with a loan advisor.

What Is a VA Loan?

A VA loan is a mortgage program guaranteed by the U.S. Department of Veterans Affairs, enabling eligible military service members, veterans, and qualifying surviving spouses to purchase homes or refinance existing mortgages with favorable terms. Unlike conventional financing that typically requires substantial initial investments, VA loans allow qualified borrowers to explore flexible funding options that minimize upfront cash requirements beyond closing costs.

The VA doesn't lend money directly—instead, it guarantees a portion of each loan, protecting approved lenders against losses if borrowers default. This guarantee eliminates the need for private mortgage insurance, reduces lender risk, and enables more favorable terms than comparable conventional financing options.

How do VA loans differ from conventional mortgage programs?

VA loans provide several distinct advantages for eligible military families:

- Flexible initial investment structures - Purchase homes with competitive equity options designed specifically for military borrowers

- No private mortgage insurance - Eliminate ongoing mortgage insurance premiums that conventional borrowers typically pay

- Competitive market pricing - Access favorable structures often better than conventional alternatives

- Flexible credit standards - Qualify with varied credit profiles that might challenge conventional approval

- Limited closing costs - Benefit from restrictions on fees lenders can charge VA borrowers

- Assumability features - Transfer loans to qualified buyers when selling, potentially attracting more purchasers

These advantages reflect the nation's commitment to supporting those who've served in uniform by making homeownership more accessible and affordable.

See how other military families have successfully used VA financing:

- View VA loan purchase case studies

- View VA loan refinance case studies

- View VA loan cash-out refinance case studies

- View VA IRRRL case studies

- View VA construction loan case studies

Who Qualifies for VA Loans?

VA loan eligibility centers on military service requirements, creditworthiness, and income sufficiency. Understanding these requirements helps determine whether this financing option fits your circumstances.

Military Service Requirements

What service qualifications make borrowers eligible for VA loans?

VA loan eligibility extends to multiple categories of current and former military personnel:

Active duty service members who have served:

- 90 continuous days during wartime periods

- 181 days during peacetime

- Any duration if discharged due to service-connected disability

Veterans who completed:

- 90 days of active service during wartime with honorable discharge

- 181 days during peacetime with honorable discharge

- 6 years in National Guard or Reserves with honorable discharge

- Any service period if discharged due to service-connected disability

National Guard and Reserve members who have:

- Completed 6 years of service in Selected Reserve or National Guard

- Been discharged honorably or continue serving

- Completed required drills and annual training periods

Surviving spouses who:

- Lost a spouse in service or from service-connected disabilities

- Have not remarried (or remarried after age 57)

- Receive Dependency and Indemnity Compensation

Specific service period requirements vary based on when you served. The VA eligibility requirements page provides detailed timelines for different service eras.

Certificate of Eligibility Process

How do you obtain a Certificate of Eligibility for VA loans?

Before applying for VA financing, you need a Certificate of Eligibility (COE) documenting your qualification. Obtain your COE through:

- Online application via the VA's eBenefits portal using your DS Logon credentials

- Through your lender who can request your COE electronically during the application process

- Mail application by submitting VA Form 26-1880 with supporting military documentation

- In-person request at local VA regional offices with appropriate service records

Required documentation varies by service category:

- Veterans: DD Form 214 (Certificate of Release or Discharge from Active Duty)

- Active duty: Statement of Service signed by commander, adjutant, or personnel officer

- Reservists/Guard: DD Form 214 plus points statement showing qualifying service

- Surviving spouses: Marriage certificate, veteran's DD Form 214, and VA death letter

Most borrowers obtain COEs within minutes through online applications or lender requests. Paper applications typically process within 5-10 business days.

Income and Credit Requirements

What financial qualifications must VA loan applicants meet?

Beyond military eligibility, VA loans require sufficient income to support mortgage obligations and reasonable credit history:

Income sufficiency - Demonstrate stable, predictable income that comfortably covers:

- Proposed housing expenses including principal, interest, taxes, and insurance

- Existing debt obligations such as car loans, student loans, and credit cards

- Living expenses appropriate for your family size and geographic location

Credit standards - Maintain responsible credit management including:

- Payment patterns showing consistent on-time obligations

- Resolution of any past credit issues with satisfactory explanations

- Reasonable recent credit activity without excessive new accounts

- Overall creditworthiness supporting long-term mortgage commitments

Residual income - Meet VA's unique residual income requirements that calculate remaining funds after subtracting all monthly obligations. These requirements vary by:

- Family size (more members require higher residual income)

- Geographic region (higher cost areas have elevated thresholds)

- Loan amount (larger mortgages need greater residual capacity)

The VA's residual income approach provides more realistic affordability assessment than conventional debt ratios alone, recognizing that families need adequate funds for utilities, food, transportation, and emergencies beyond just paying debts.

Calculate your personalized scenarios with these tools:

- VA loan purchase calculator

- VA loan refinance calculator

- VA loan cash-out refinance calculator

- VA IRRRL calculator

- VA construction loan calculator

Understanding VA Loan Entitlement

What is VA loan entitlement and how does it work?

VA loan entitlement represents the amount the VA guarantees to lenders if a borrower defaults. This guarantee protects lenders and enables them to offer favorable terms without requiring private mortgage insurance or substantial initial investments.

Basic Entitlement vs. Bonus Entitlement

The VA provides two layers of entitlement:

Basic entitlement - The initial guarantee amount available to all eligible veterans, which covers a portion of the loan amount

Bonus entitlement - Additional guarantee capacity that extends coverage for higher loan amounts in more expensive housing markets

Combined, these entitlement tiers enable qualified borrowers to purchase homes at various price points across different markets without initial equity contributions, provided they meet income and credit standards.

Using Entitlement Multiple Times

Can you use VA loan benefits more than once?

Yes. Veterans can use VA loan benefits multiple times throughout their lives. Your entitlement restores after:

- Selling a property financed with a VA loan and paying off the mortgage completely

- Having another qualified veteran assume your existing VA loan

- Requesting one-time restoration if you've repaid a previous VA loan but still own the property

Even with partial entitlement in use, many veterans retain sufficient remaining entitlement to purchase additional properties. The VA entitlement information page provides detailed guidance on calculating available entitlement and restoration processes.

Entitlement for Multiple Properties

Veterans with sufficient entitlement can hold multiple VA loans simultaneously. This flexibility benefits military families who:

- Purchase new primary residences before selling previous homes

- Maintain former primary residences as rental properties while relocating

- Own vacation homes in locations where they plan to retire

Each property must meet VA occupancy requirements at the time of purchase, but you can convert former primary residences to rentals after establishing occupancy.

CHECKPOINT #1 - Re-reading REG Z compliance section before Key Details...

VA Loan Funding Fees

What is the VA funding fee and who pays it?

The VA funding fee helps sustain the loan program for future generations of military borrowers. This one-time charge varies based on several factors:

Service category - Regular military, Reserves, and National Guard members pay different amounts

Loan purpose - Purchase loans, refinances, and subsequent uses have varied fee structures

Initial investment amount - Larger equity contributions reduce the funding fee percentage

Disability status - Veterans receiving VA disability compensation are exempt from funding fees entirely

Most borrowers finance the funding fee into their loan amount rather than paying it at closing, spreading the cost over the life of the mortgage. Use the VA funding fee chart to determine your specific fee based on your circumstances.

Funding Fee Exemptions

Who qualifies for VA funding fee waivers?

Several categories of veterans avoid funding fees entirely:

- Veterans receiving VA disability compensation for service-connected disabilities

- Veterans eligible to receive disability compensation but receiving retirement pay instead

- Surviving spouses receiving Dependency and Indemnity Compensation

- Service members awarded the Purple Heart

Funding fee exemptions provide significant savings, potentially reducing overall loan costs by thousands of dollars depending on the loan amount.

Types of VA Loans Available

The VA loan program includes several specialized options serving different borrowing needs. Understanding each type helps you select the most appropriate financing for your situation.

VA Purchase Loans

How do VA purchase loans work for buying homes?

VA purchase loans enable eligible military families to buy primary residences with competitive terms and flexible initial investment options. These loans work for:

- Single-family homes that meet VA property condition standards

- Condominiums in VA-approved projects

- Manufactured homes meeting HUD code and permanent foundation requirements

- New construction homes built to local building codes

VA purchase loans require properties to meet minimum property requirements ensuring homes are safe, sound, and sanitary. Properties must be move-in ready without significant repairs or safety hazards.

View VA loan purchase case studies to see how other military families have used this financing successfully.

VA Refinance Loans (Rate-and-Term)

When should you consider a standard VA refinance?

VA rate-and-term refinances allow you to replace existing mortgages with new VA loans that may offer better terms. This option works particularly well when you:

- Currently have an FHA, conventional, or other non-VA mortgage you want to convert to VA financing

- Want to eliminate private mortgage insurance required on conventional loans

- Need to add or remove a spouse from the loan due to marriage, divorce, or inheritance situations

- Seek to adjust your loan structure to better fit current circumstances

Unlike the streamlined IRRRL (discussed below), standard VA refinances require:

- Full income and credit documentation

- New property appraisal

- Complete underwriting review

- Certificate of Eligibility verification

However, standard VA refinances offer advantages the IRRRL doesn't provide:

- Ability to receive funds back at closing (typically up to a certain amount)

- Option to add or remove borrowers from the loan

- Capacity to refinance non-VA loans into VA financing

- Opportunity to eliminate private mortgage insurance from conventional loans

View VA loan refinance case studies to explore real scenarios where this option made financial sense.

VA Cash-Out Refinance Loans

How do VA cash-out refinances provide access to home equity?

VA cash-out refinances let you tap into accumulated home equity by refinancing for more than your current mortgage balance. The difference converts to cash you can use for:

- Home improvements or renovations that increase property value

- Debt consolidation that simplifies finances and potentially reduces overall interest costs

- Major expenses such as education costs or medical bills

- Emergency reserves providing financial security

- Investment opportunities or business capital needs

VA cash-out refinances work with any existing mortgage type—whether VA, FHA, conventional, or others. You need:

- Adequate equity in your property based on current appraised value

- Sufficient income to support the new, larger loan amount

- Acceptable credit standing with responsible payment history

- Primary residence occupancy (you must currently live in the home)

The funding fee for cash-out refinances differs from purchase loans and standard refinances, so factor this cost into your decision-making process.

View VA cash-out refinance case studies to understand when accessing equity makes strategic sense.

VA Interest Rate Reduction Refinance Loan (IRRRL)

What makes the VA IRRRL different from standard VA refinances?

The IRRRL (Interest Rate Reduction Refinance Loan), also called the VA Streamline Refinance, provides a simplified path to refinance existing VA loans. This specialized option offers:

Streamlined processing - Minimal documentation requirements compared to standard refinances

No appraisal required - Most IRRRLs proceed without new property valuations

Reduced verification - Limited income and credit review in many circumstances

Quick closings - Faster processing timelines due to simplified requirements

Lower funding fees - Reduced fee structure compared to other VA loan types

The IRRRL serves one primary purpose: reducing your interest costs on an existing VA loan. Key restrictions include:

- Must currently have a VA loan (cannot refinance FHA, conventional, or other loan types)

- Must lower your interest expense or move from an adjustable rate to a fixed rate

- Cannot add or remove borrowers from the loan

- Limited cash back at closing (typically capped at a minimal amount)

- Must certify previous occupancy of the property

Use an IRRRL when you want to reduce your existing VA loan costs quickly and simply. Choose a standard VA refinance when you need more flexibility to modify loan terms, access equity, or change borrowers.

View VA IRRRL case studies to see simplified refinancing in action.

VA Construction Loans

Can you use VA benefits to build a new home?

VA construction loans combine land purchase and construction financing in a single-close transaction, enabling eligible military families to build custom homes with competitive VA terms. These specialized loans cover:

- Land acquisition costs if you don't already own the property

- Construction expenses for building your primary residence

- Permanent financing that activates after construction completes

- Builder and contractor costs meeting VA approval standards

VA construction loans require:

- Detailed construction plans and specifications

- Licensed, insured contractors with acceptable track records

- Construction budgets and timelines meeting VA guidelines

- Properties in locations where you'll establish primary residence

The construction-to-permanent structure provides certainty throughout the building process—you lock in your permanent financing terms before construction begins, avoiding refinancing risks after project completion.

View VA construction loan case studies to explore how military families build custom homes using VA benefits.

Ready to discuss your specific situation? Submit a purchase inquiry to explore your options.

VA Loan Property Requirements

What property standards must homes meet for VA financing?

The VA mandates minimum property requirements (MPRs) ensuring homes are safe, sound, and sanitary. These standards protect both veterans and the VA by preventing financing of properties with significant defects or safety hazards.

Minimum Property Requirements

VA appraisers evaluate properties against specific criteria:

Structural soundness - Homes must have solid foundations, intact roofs, and stable structural systems without significant damage or deterioration

Safe electrical systems - Wiring must meet local codes without fire hazards or safety risks

Adequate heating - Properties require permanent heating systems capable of maintaining comfortable temperatures in living areas

Clean water supply - Homes need access to potable water meeting local health standards

Functional plumbing - Properties must have working plumbing systems including adequate bathroom facilities

Pest-free conditions - Homes cannot have active termite or pest infestations requiring treatment

Safe access - Properties require legal access via public roads or easements

Proper drainage - Sites must have adequate drainage preventing water accumulation or foundation damage

Common Property Issues

What property problems prevent VA loan approval?

Several conditions typically require correction before VA financing approval:

- Missing or damaged roofing that compromises weather protection

- Peeling paint on homes built before 1978 due to lead-based paint concerns

- Non-functioning mechanical systems including heating, cooling, or water heaters

- Inadequate electrical capacity or unsafe wiring configurations

- Termite damage requiring structural repairs

- Foundation cracks or settlement suggesting structural instability

- Missing handrails on stairs or inadequate guardrails on elevated decks

- Contaminated water supplies failing quality testing

Sellers typically address these issues through repairs before closing. Alternatively, VA renovation loans can include repair costs in the financing, though this approach adds complexity to the transaction.

Acceptable Property Types

What types of properties qualify for VA financing?

VA loans work for several property categories:

- Single-family homes including detached houses, townhomes, and duplexes where you occupy one unit

- Condominiums in VA-approved projects meeting specific organizational and financial standards

- Manufactured homes built to HUD standards and permanently affixed to foundations

- New construction built by licensed contractors following local building codes

VA loans generally don't finance:

- Investment properties you won't occupy as your primary residence

- Vacation homes used seasonally rather than year-round

- Properties requiring substantial rehabilitation before occupancy

- Co-ops and some condominium projects not meeting VA approval standards

- Commercial properties or mixed-use buildings with significant commercial space

Common Questions About VA Loans Mid-Journey

Can You Use a VA Loan to Buy Investment Property?

No. VA loans require borrowers to occupy properties as primary residences. You must move into the home within 60 days of closing and maintain it as your primary residence for at least one year, barring extraordinary circumstances like military orders.

However, you can convert former primary residences to rental properties after meeting the occupancy requirement. This flexibility helps military families who relocate frequently—you can purchase a new primary residence with a VA loan while retaining and renting your previous home.

How Long Does VA Loan Approval Take?

What timeline should borrowers expect for VA loan processing?

VA loan approval timelines vary based on loan type and application complexity:

Purchase loans typically close in 30-45 days from application to closing, including:

- Application and documentation submission (3-5 days)

- VA appraisal ordering and completion (7-14 days)

- Underwriting review and conditional approval (7-14 days)

- Condition clearing and final approval (5-10 days)

- Closing preparation and scheduling (3-5 days)

IRRRLs often process faster, sometimes closing within 20-30 days due to streamlined documentation and limited appraisal requirements.

Cash-out refinances and standard refinances typically require 30-45 days similar to purchase loans.

Starting the process early, maintaining organized documentation, and responding promptly to lender requests accelerates timelines.

Do VA Loans Have Income Limits?

No. Unlike some government programs, VA loans don't impose maximum income limits. Eligibility depends on military service, not income level. However, you must demonstrate sufficient income to support your mortgage obligations and maintain adequate residual income for living expenses.

Higher incomes generally strengthen applications by demonstrating strong repayment capacity, but the VA doesn't exclude high earners from the program.

Can Self-Employed Veterans Qualify for VA Loans?

Yes. Self-employed veterans qualify for VA financing using documentation including:

- Two years of business tax returns showing income trends

- Year-to-date profit and loss statements if applying during the current tax year

- Business bank statements demonstrating regular deposits and cash flow

- CPA-prepared financial statements for complex business structures

- Business licenses and documentation proving ongoing operations

Lenders analyze self-employment income carefully, often averaging earnings across multiple years to account for natural business fluctuations. Stable or increasing income trends strengthen applications, while declining patterns may require additional explanation.

For alternative self-employment financing options:

- Bank Statement Loan - Qualifies using business bank deposits instead of tax returns

- 1099 Loan - Approves independent contractors using 1099 income documentation

- P&L Loan - Qualifies based on CPA-prepared profit and loss statements

What Credit Score Do You Need for VA Loans?

The VA doesn't mandate specific minimum credit scores, but most lenders prefer scores above 620 for streamlined processing. Veterans with lower scores may still qualify through manual underwriting examining overall credit patterns rather than relying solely on numerical scores.

Factors that strengthen applications with lower credit scores:

- Demonstrated history of timely housing payments over the past 12-24 months

- Explanations for any past credit issues with evidence of resolution

- Stable employment and income that comfortably supports proposed housing expenses

- Strong residual income exceeding VA minimum requirements

- Minimal recent credit inquiries suggesting responsible credit management

Even with qualifying scores, lenders examine complete credit profiles including payment patterns, debt levels, and recent credit activity to assess overall creditworthiness.

Can You Have Two VA Loans at the Same Time?

Is it possible to hold multiple VA loans simultaneously?

Yes, provided you have sufficient remaining entitlement. Veterans with full entitlement available can typically obtain second VA loans for new primary residences. Common scenarios include:

- Relocating for military orders before selling your previous VA-financed home

- Purchasing a new primary residence while retaining a former home as a rental

- Buying a vacation home in a location where you plan to establish primary residence

Each property must serve as your primary residence at the time of purchase, meeting the occupancy requirement. After establishing occupancy, you can convert properties to rentals while purchasing new primary residences with additional VA loans.

Calculate your available entitlement and determine whether sufficient capacity remains for multiple properties. The VA entitlement information page provides detailed guidance on using entitlement for multiple properties.

CHECKPOINT #2 - Re-reading REG Z compliance section before detailed requirements...

VA Loan Occupancy Requirements Explained

What occupancy rules apply to VA-financed properties?

VA loans require borrowers to establish properties as primary residences within 60 days of closing. This occupancy requirement ensures VA benefits serve their intended purpose—helping military families obtain primary housing, not investment properties or vacation homes.

Primary Residence Certification

At closing, borrowers certify their intent to occupy properties as primary residences. This certification represents a legal commitment that the VA takes seriously. Violation of occupancy requirements can result in:

- Loan acceleration requiring immediate full repayment

- Loss of VA loan benefits for future use

- Potential legal action for loan fraud

Legitimate exceptions exist for circumstances beyond borrower control, such as:

- Military orders requiring relocation before establishing occupancy

- Serious illness preventing physical occupancy

- Job transfers mandated by employers

- Natural disasters rendering properties uninhabitable

Document any circumstances preventing timely occupancy and communicate with your lender immediately to explore available options.

Converting to Rental Properties

Can you rent out a VA-financed property after living there?

Yes. After meeting the initial occupancy requirement (typically one year), you can convert VA-financed properties to rentals. This flexibility particularly benefits military families who relocate frequently due to permanent change of station (PCS) orders.

When converting to rental use:

- Notify your homeowner's insurance company to adjust coverage for rental property

- Understand landlord responsibilities including property maintenance and tenant relations

- Consider property management services if relocating far from the rental

- Maintain adequate financial reserves for vacancies and repairs

- Report rental income appropriately on tax returns

Many military families build substantial real estate portfolios by purchasing homes with VA loans during each relocation, then retaining and renting properties when transferring to new duty stations.

VA Loan Assumption Benefits

What makes VA loan assumability valuable?

VA loans include assumability features allowing qualified buyers to take over existing VA loans and their terms. This benefit can make properties more attractive to buyers, especially when current market conditions offer less favorable terms than your existing loan.

How VA Loan Assumptions Work

When you sell a VA-financed property, qualified buyers can assume your existing loan by:

- Meeting lender qualification standards including income verification and credit review

- Paying any difference between the loan balance and purchase price

- Completing assumption processing through the existing lender

- Paying assumption fees which are typically modest compared to new loan costs

Buyers assuming VA loans benefit from:

- Avoiding new loan origination processes and associated costs

- Potentially securing better terms than current market offerings

- Faster closing timelines compared to new loan applications

Releasing Liability Through Assumptions

Does selling remove your obligation on assumed VA loans?

Not automatically. When buyers assume your VA loan, you remain liable unless you obtain formal liability release from the lender. To release liability:

- The assuming buyer must be a qualified veteran or service member (preferred path to release entitlement)

- The buyer must meet standard VA loan approval criteria

- The lender must approve the assumption and grant formal liability release

If a non-veteran assumes your loan, you typically remain liable even after selling. If that buyer later defaults, the VA could pursue you for any losses. Always seek formal liability release when allowing loan assumptions.

Additionally, your VA entitlement remains tied to the assumed loan until either:

- You obtain formal entitlement release (typically requires a veteran to assume)

- The assuming buyer pays off the loan completely

- You request one-time restoration after repaying the loan yourself

Explore all loan programs to understand your complete range of options.

Advanced VA Loan Topics

Can You Use a VA Loan to Buy a Multi-Unit Property?

Do VA loans finance properties with multiple units?

Yes. VA loans can finance properties with up to four units, provided you occupy one unit as your primary residence. This option enables veterans to:

- Build equity while collecting rental income from additional units

- Offset housing costs with tenant payments

- Create long-term real estate investments

- Establish residual income from property ownership

Multi-unit properties must meet VA minimum property requirements for all units, not just your occupied space. Each unit requires:

- Separate entrance access (shared interior access may not qualify)

- Independent utility systems or properly divided shared utilities

- Compliance with local zoning for multi-family use

- Adequate parking for all units

Lenders typically use rental income from additional units when calculating qualifying income, strengthening your ability to afford larger properties. However, they usually discount expected rental income by a certain percentage to account for vacancies and expenses.

What Happens If You Didn't Live in the Property as Required?

Failing to meet VA occupancy requirements represents a serious issue with potential consequences:

Immediate concerns:

- Lender may call the loan due, requiring immediate full repayment

- VA may withdraw loan guarantee, exposing lender to losses

- Your VA loan eligibility could be suspended or revoked

- Potential prosecution for loan fraud in egregious cases

If you cannot establish occupancy due to legitimate circumstances:

- Contact your lender immediately explaining the situation

- Provide documentation supporting why occupancy isn't possible

- Explore potential remedies including occupancy extensions or loan modification

- Consider selling the property to avoid compliance violations

The VA recognizes that unexpected circumstances sometimes prevent occupancy. Early communication and honest disclosure typically lead to workable solutions, while attempting to hide occupancy violations creates far more serious problems.

How Do VA Loans Work for Native American Veterans?

What special provisions exist for Native American veterans?

The VA offers a specialized program called the Native American Direct Loan (NADL) program serving veterans who are Native American or married to Native Americans. This program enables:

- Purchases, construction, or improvements on Federal Trust Land

- Direct lending from the VA (not through private lenders)

- Flexible terms similar to standard VA loan programs

- Limited availability based on Congressional funding and VA resources

The NADL program addresses unique challenges Native Americans face accessing traditional financing on trust lands where fee-simple ownership doesn't exist. Not all tribes participate in the program—check with the VA Native American Direct Loan program for current participating tribes and availability.

Can You Get a VA Loan After Bankruptcy or Foreclosure?

How do past credit issues affect VA loan eligibility?

The VA doesn't prohibit financing for veterans with previous bankruptcies or foreclosures, though waiting periods and seasoning requirements apply:

After Chapter 7 bankruptcy:

- Typically wait two years from discharge date

- Demonstrate reestablished credit with responsible payment patterns

- Show stable income and employment since bankruptcy

- Provide explanation of circumstances leading to bankruptcy

After Chapter 13 bankruptcy:

- May qualify after 12 months of on-time plan payments with trustee approval

- Must demonstrate financial recovery and responsible credit management

- Show ability to handle mortgage obligations while completing bankruptcy plan

After foreclosure:

- Generally wait two years from foreclosure completion

- Reestablish credit demonstrating financial recovery

- Provide explanation and evidence of circumstances beyond your control

- Show stable employment and income since foreclosure

Lenders may impose stricter requirements beyond VA minimums. Previous VA loan foreclosures require additional considerations and potentially longer waiting periods.

What Documentation Do You Need for VA Loans?

What paperwork is required for VA loan applications?

Comprehensive documentation requirements include:

Military service documentation:

- Certificate of Eligibility (COE) obtained through VA or your lender

- DD Form 214 for veterans (or Statement of Service for active duty)

- Proof of current military status for active duty applicants

Income verification:

- Two years of federal tax returns with all schedules

- Recent pay stubs covering 30 days for employed applicants

- W-2 forms from the past two years

- Documentation of any additional income including retirement, disability, or investment income

Self-employment documentation (if applicable):

- Two years of business tax returns including all schedules

- Year-to-date profit and loss statements

- Business bank statements

- CPA-prepared financials for complex businesses

Asset verification:

- Bank statements from all accounts spanning 60 days

- Retirement account statements

- Documentation of any gift funds or non-employment income sources

Credit and identity:

- Valid government-issued identification

- Social Security card

- Authorization for credit report inquiries

- Written explanations for any credit issues

Organized, complete documentation accelerates processing and reduces delays from missing information or unclear circumstances.

How Do VA Loans Handle Gift Funds?

Can family members contribute funds toward VA loan purchases?

Yes. VA loans allow gift funds from acceptable sources to cover closing costs or other transaction expenses. Acceptable gift donors include:

- Family members including parents, grandparents, siblings, and adult children

- Employers providing relocation assistance or housing benefits

- Close friends with clearly established relationships

- Labor unions or employer-affiliated organizations

- Government agencies or charitable organizations

Gift documentation requires:

- Written gift letter stating the amount, source, and relationship

- Confirmation that gifts don't require repayment

- Evidence of donor's ability to provide the gift

- Documentation showing gift fund transfer to your accounts

Lenders verify gift funds carefully to ensure they represent true gifts rather than disguised loans that would increase your debt obligations. Gifts must be fully transferred before closing, and you'll need to maintain documentation proving the source.

Comparing VA Loans to Other Financing Options

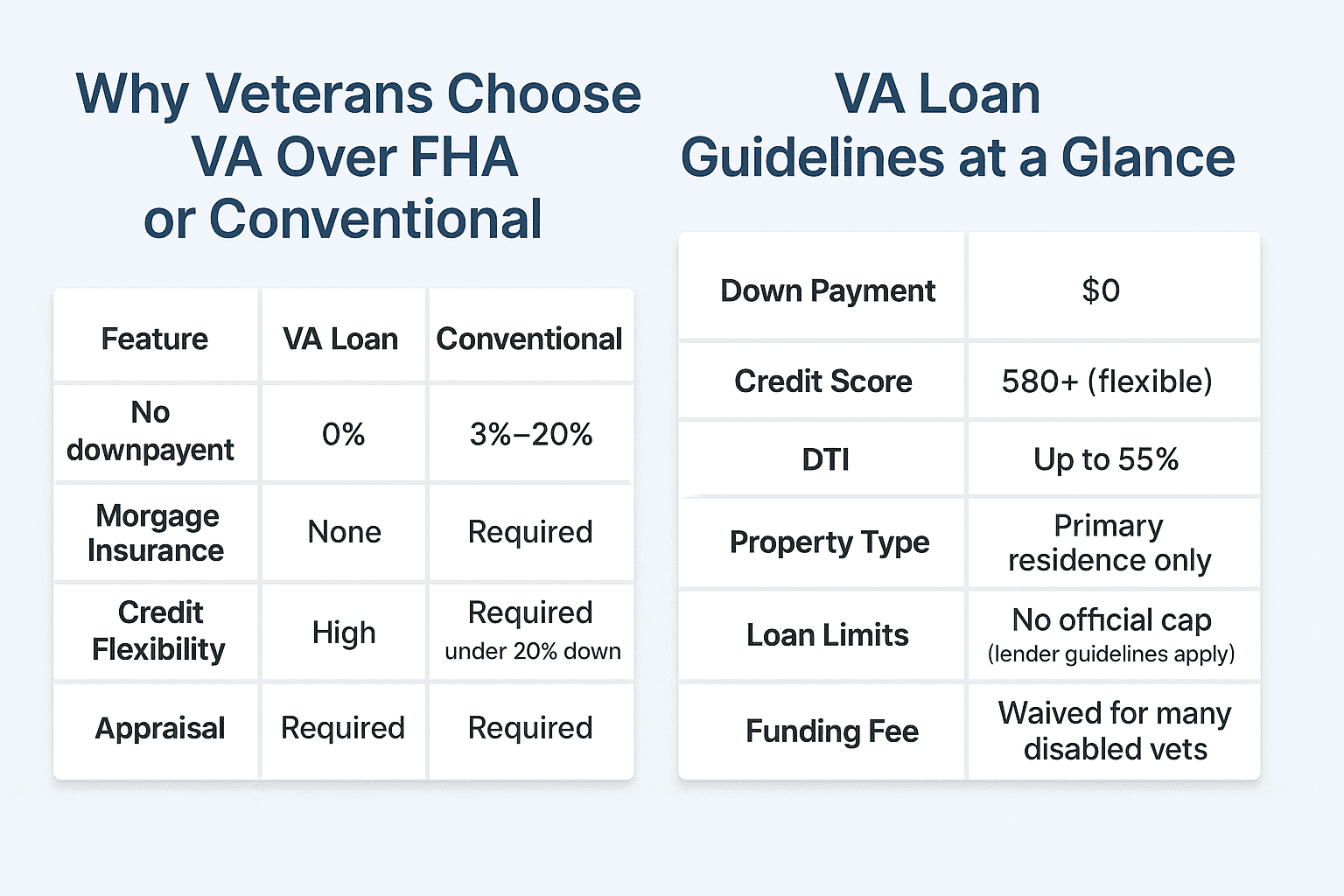

VA Loans vs. FHA Loans

How do VA and FHA loans differ?

Both programs serve borrowers who might struggle with conventional financing, but key differences include:

Initial investment requirements:

- VA: Flexible equity structures with competitive options

- FHA: Various funding alternatives available

Mortgage insurance:

- VA: No private mortgage insurance requirements

- FHA: Ongoing mortgage insurance required regardless of equity level

Property standards:

- VA: Minimum property requirements focused on safety and soundness

- FHA: Similar safety standards with specific HUD requirements

Eligibility:

- VA: Restricted to qualifying military service members and veterans

- FHA: Available to all borrowers meeting program requirements

Assumability:

- VA: Loans are assumable by qualified buyers

- FHA: Loans are also assumable but with different requirements

VA loans typically provide better overall value for eligible military families due to the absence of mortgage insurance and competitive structures.

VA Loans vs. Conventional Loans

When should veterans choose conventional financing over VA loans?

Most eligible veterans benefit from using VA loans, but conventional financing sometimes makes sense when:

- Purchasing properties exceeding VA loan limits in high-cost areas

- Buying investment properties not qualifying for VA financing

- Preferring to avoid VA funding fees when making larger equity contributions

- Purchasing condominiums in projects not meeting VA approval standards

Conventional loans offer:

- No VA appraisal requirements or minimum property standards

- Faster processing timelines in some circumstances

- Flexibility for investment property purchases

- No funding fee requirements

However, conventional loans typically require:

- Larger initial investments for optimal terms

- Private mortgage insurance unless contributing significantly

- Higher credit standards in many circumstances

- Less flexibility for borrowers with past credit issues

Calculate scenarios using both loan types to determine which approach provides better overall value for your specific situation.

Considering a refinance? Submit a refinance inquiry to see if this makes sense for you.

Final VA Loan Questions

Can VA Loans Finance Condominiums?

What condominium requirements apply to VA financing?

VA loans can finance condominiums, but projects must meet VA approval standards covering:

Financial stability - The condo association must maintain adequate reserves and demonstrate sound financial management

Owner-occupancy ratios - A minimum percentage of units must be owner-occupied rather than rented

Project completion - New construction projects must reach specific completion thresholds before individual unit financing

Legal structure - Projects must have appropriate legal formation with proper documentation

Insurance coverage - Associations must carry adequate hazard and liability insurance

Check the VA condominium approval database to verify whether specific projects qualify before making purchase offers. Not all condominiums meet VA standards, so verification prevents wasted time on properties that won't qualify.

How Do VA Loans Handle Manufactured Homes?

Can you use VA benefits for manufactured housing?

Yes, but manufactured homes must meet specific requirements:

- Built to HUD Manufactured Home Construction and Safety Standards (HUD code)

- Constructed after June 15, 1976 when current HUD standards took effect

- Classified and titled as real property, not personal property

- Permanently affixed to land you own (not leased lots)

- Built on a permanent foundation meeting local codes

- Minimum square footage typically exceeding 400 square feet

- Width exceeding 40 feet for double-wide units

The land and manufactured home must be purchased together in a single transaction. VA loans don't finance manufactured homes on leased land or in manufactured home communities where you don't own the lot.

What Are VA Loan Limits?

Do VA loans cap financing amounts?

For veterans with full entitlement, VA loans generally don't impose maximum loan amounts. You can borrow whatever amount lenders approve based on your income and credit qualifications.

However, the concept of "loan limits" still matters for:

Veterans with partial entitlement - If you've used VA benefits previously without restoring full entitlement, limits apply based on remaining entitlement capacity

Conforming loan limits - Properties exceeding local conforming loan limits may require some initial investment to avoid second-tier liens

Lender policies - Individual lenders may impose their own maximum loan amounts based on risk management preferences

In high-cost areas, veterans can finance expensive properties without any equity contribution, provided their income supports the mortgage obligations and they have full entitlement available.

Can You Refinance a VA Loan Into a Conventional Loan?

Yes. Veterans can refinance VA loans into conventional financing when this strategy makes sense. Reasons to consider this include:

- Eliminating the VA funding fee if you plan to refinance again soon

- Accessing conventional renovation loan programs for major improvements

- Simplifying loan transfer if selling to non-veteran buyers

- Preserving full VA entitlement for purchasing another property

However, refinancing to conventional financing usually means:

- Adding private mortgage insurance unless you have substantial equity

- Potentially accepting less favorable terms than your VA loan offers

- Losing VA loan benefits including flexible qualification and assumability

Calculate both scenarios carefully before converting VA loans to conventional financing. In most cases, VA loans provide better long-term value for eligible veterans.

How Does Divorce Affect VA Loans?

What happens to VA loans during divorce proceedings?

Divorce complicates VA loan situations in several ways:

If both spouses signed the loan:

- Both remain legally obligated regardless of divorce agreements

- Divorce decrees don't override mortgage contract obligations

- The VA remains liable based on the original loan terms

Options for resolution:

- Refinance to remove one spouse - The spouse keeping the home refinances in their name alone using a standard VA refinance or conventional loan

- Sell the property - Both spouses satisfy their obligations by selling and paying off the mortgage

- One spouse assumes the loan - Some lenders allow qualified spouses to formally assume the loan, releasing the other spouse from liability

- Continue co-borrowing - Both maintain the loan despite divorce, though this creates ongoing financial entanglement

Entitlement considerations:

- If your ex-spouse keeps a home financed with your joint VA loan, your entitlement may remain tied to that property

- You might need to request substitution of entitlement or wait until the property sells to restore full benefits

Consult with both your divorce attorney and mortgage professionals to understand implications and develop the best strategy for your circumstances.

What Properties Don't Qualify for VA Financing?

What types of properties can't use VA loans?

Several property categories don't meet VA financing requirements:

- Properties you won't occupy as primary residences

- Vacation homes used seasonally or recreationally

- Investment properties purchased specifically for rental income

- Raw land without improvements or construction plans

- Properties with active code violations or condemnation orders

- Homes requiring substantial rehabilitation before occupancy

- Properties with commercial use exceeding allowable thresholds

- Co-operative apartment buildings with proprietary leases

- Properties located outside the United States and its territories

Some property types require specialized VA loan programs—like manufactured homes needing HUD code compliance, or Native American veterans purchasing on trust lands needing the NADL program.

How Do You Restore VA Loan Entitlement?

What steps restore VA benefits after previous use?

Restore full VA loan entitlement by:

One-time restoration without selling - Available once if you've repaid a previous VA loan but still own the property, allowing you to use benefits again while retaining the first home

Full restoration after selling - Automatically restores when you sell VA-financed properties and pay off the loans completely

Restoration through assumption - Regain entitlement when qualified veterans assume your existing VA loans with formal substitution of entitlement

Required documentation:

- Evidence showing the previous VA loan was paid in full

- Property sale documentation if applicable

- VA Form 26-1880 (Certificate of Eligibility application)

- Previous loan information including lender details and payoff date

Most entitlement restorations process quickly through the VA's electronic systems. Submit your request as soon as you've satisfied previous VA loans to ensure benefits are available when you need them.

Can National Guard and Reserve Members Use VA Loans?

What requirements apply to Guard and Reserve members?

Yes, National Guard and Reserve members qualify for VA loans after completing six years of service. Specific requirements include:

Active Reserve or Guard service including:

- Attending required monthly drill periods

- Completing annual training requirements

- Maintaining satisfactory participation records

- Receiving honorable characterization of service

Alternative qualification paths:

- Active duty service for qualifying periods

- Deployment to active duty during wartime or contingency operations

- Service-connected disability discharge at any point

Guard and Reserve members obtain Certificates of Eligibility the same way as regular military veterans, using DD Form 214 plus points statements showing total qualifying service time.

Ready to get started? Apply now or schedule a call to discuss your situation.

Alternative Loan Programs for Military Families and Home Buyers

If a VA loan isn't the right fit, consider these alternatives:

- FHA Loan - Government-backed financing with flexible qualification standards and various initial investment options for all borrowers

- Conventional Loan - Traditional financing offering flexibility for various property types and purchase scenarios

- USDA Loan - Rural housing financing with competitive terms for properties in eligible areas

- Jumbo Loan - Financing for properties exceeding conforming loan limits in high-cost markets

- Renovation Loan - Combined purchase and improvement financing for properties needing repairs or upgrades

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

Helpful VA Loan Resources

Official Government Guidance

VA Home Loans Overview and Benefits - Comprehensive Department of Veterans Affairs resource explaining loan program benefits, eligibility requirements, and application processes for all VA financing options.

VA Loan Eligibility Requirements - Official eligibility criteria detailing service requirements for active duty members, veterans, National Guard, Reserves, and surviving spouses.

VA Funding Fee Chart and Exemptions - Current funding fee schedules showing amounts based on service type, loan purpose, and initial investment levels, plus exemption criteria.

VA Certificate of Eligibility Application - Online portal for veterans to obtain Certificates of Eligibility electronically through the eBenefits system.

Property and Appraisal Standards

VA Minimum Property Requirements - Detailed standards covering property condition requirements, appraisal processes, and minimum acceptable property characteristics.

VA Condominium Approval Database - Searchable database of VA-approved condominium projects nationwide, updated regularly as projects gain or lose approval status.

Educational Resources

Consumer Financial Protection Bureau Mortgage Guide - Federal consumer protection agency providing unbiased information about mortgage financing, closing processes, and borrower rights applicable to all loan types.

HUD Housing Counseling Services - Directory of HUD-approved housing counselors offering free or low-cost assistance with mortgage questions, financial planning, and homeownership education.

Military Family Resources

Military OneSource Financial Resources - Department of Defense program offering free financial counseling, education, and resources specifically for military families navigating home purchases and mortgages.

Defense Finance and Accounting Service - Official military pay information and resources helping service members document income for mortgage applications.

Need a Pre-Approval Letter—Fast?

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

- Only 2 minutes to complete

- Quick turnaround on pre-approval

- No credit score impact

Got a Few Questions First?

Let’s talk it through. Book a call and one of our friendly advisors will be in touch to guide you personally. Schedule A CallNot Sure About Your Next Step?

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

- Takes just 5 minutes

- Tailored results based on your answers

- No credit check required